Risk Warning

The contents of this article are intended strictly for educational and risk-awareness purposes regarding cryptocurrency knowledge and do not constitute any investment advice, trading advice, financial advice, legal advice, or tax advice. IDOs, IEOs, ICOs, new token subscriptions, on-chain public rounds, and early-stage token investments are all extremely high-risk activities that can lead to severe principal losses or even total capital loss. Please make independent judgments only after fully understanding a project's background, tokenomics model, vesting schedules, smart contract risks, and your local regulatory requirements.

In the cryptocurrency market, many people hear the term "IDO" for the first time because a certain project "surged 10x on its first day of listing," "whitelist users made dozens of times their money," or "early participants secured cheap chips."

These stories certainly exist, but they only showcase the most attractive side of IDOs. They gloss over the flip side: a massive number of IDO projects plunge below their issuance price immediately upon listing, lose 80% or even 95% of their value within 3 to 6 months, stop updates completely, leave their communities abandoned, experience a total freeze in liquidity, and ultimately trend toward zero.

Therefore, truly understanding an IDO requires more than knowing it stands for Initial DEX Offering or that it means "token issuance on a decentralized exchange." It requires a deep understanding of how the crypto fundraising model has evolved:

- Why did ICOs explode, and why did they crash?

- Why did IEOs once thrive, and why did they cool down?

- What exact problems did IDOs solve, and what new risks did they introduce?

- How should retail investors participate, and how can they dodge traps?

This article will map out the historical trajectory from traditional IPOs to ICOs, IEOs, and IDOs, systematically breaking down IDO execution mechanics, the Launchpad ecosystem, participant workflows, centralized alternatives, project-specific risks, regulatory landscapes, and common beginner mistakes.

Chapter 1: Why Does the Crypto World Need Its Own Fundraising Methods? The Core Breakdown Between IPOs and On-Chain Financing

1.1 Why Are Traditional IPOs Ill-Suited for Crypto Projects?

An IPO, or Initial Public Offering, is the primary avenue for a traditional company to access public capital markets. A company builds its business over years, hires investment banks, legal counsels, and public accountants to complete audits, roadshows, and regulatory filings, lists on a legacy stock exchange, and finally allows public investors to purchase equity.

While an IPO is a highly standardized financing and exit mechanism for mature corporations, it presents three natural barriers for early-stage crypto projects:

- High Regulatory Barriers: Most early-stage crypto projects lack the mature corporate structures, revenue histories, corporate governance models, and audited financial statements required to clear traditional IPO standards.

- Rigid Geographic Fragmentation: IPO frameworks are inherently bound to specific countries or exchanges (such as Wall Street, the Hong Kong Stock Exchange, or the Singapore Exchange). Crypto projects, by contrast, serve a global user base from day one, with developers, communities, and node operators scattered internationally.

- Prohibitive Time Costs: Blockchain technology moves at a breakneck speed, where market opportunities can open and shut within months. A traditional IPO can require years of preparation, which does not match the rapid execution loops of the crypto ecosystem.

Consequently, the crypto industry naturally sought out an alternative fundraising model that is faster, globally accessible, and built specifically for a token-based economy.

1.2 How Do the Capital Needs of Blockchain Projects Differ from Traditional Tech Firms?

When a traditional tech startup raises capital, it typically sells equity. Investors purchase a claim on the company’s future net cash flows and corporate equity value.

Blockchain projects operate under a completely different paradigm. Many protocols do not start as structured corporations; instead, they function around protocols, decentralized networks, open-source communities, and native token economics.

What do they need funding for?

- Auditing and developing complex smart contracts;

- Building public base-layer blockchains or dApp protocols;

- Providing early user bootstrapping incentives;

- Funding initial liquidity pool deepness;

- Attracting external developer talent via ecosystem grants;

- Launching and maintaining global node infrastructures;

- Bootstrapping decentralized governance (DAOs);

- Building out global social media communities;

- Gaining listings on liquid trading venues.

Under this model, the token is far more than a pure capital-raising mechanism. It can represent utility access rights to the network, governance voting shares, network security incentives, native fee payment tokens, or coordination tools for automated liquidity. This is why crypto projects favor token-based fundraising over traditional venture equity.

1.3 The Ideology of "Decentralized" Capital: Why Founders Bypass Traditional Gatekeepers

The traditional financial landscape is guarded by a heavy stack of centralized gatekeepers:

- Investment banks

- Centralized brokerages and exchanges

- Government regulatory boards

- Corporate legal firms

- Auditing agencies

- Venture capital firms

- Institutional market makers

- Listing compliance committees

While these gatekeepers provide oversight and theoretical investor protections, they also introduce steep financial overhead, slow execution speeds, and high barriers to entry.

The early thesis of the crypto space asked a simple question: If the internet allowed information to break free from borders and flow globally, can blockchain technology do the same for capital and ownership?

As a result, crypto founders choose to bypass legacy financial gatekeepers to interface directly with a global community. Users are no longer just passive consumers of a software product; they become early protocol participants, token holders, community evangelists, and governance node operators.

This ideology unlocks immense grassroots innovation, but it introduces parallel risks. The innovation allows everyday retail users to access early-stage opportunities previously reserved for institutional elites. The risk is that without an institutional screening barrier, malicious actors can deploy fraudulent projects using the exact same mechanisms.

1.4 The Core Friction of Crypto Fundraising: Velocity vs. Fraud Prevention

The historical evolution of crypto fundraising has always been a battle to balance two competing forces: the need for projects to raise capital quickly and globally with minimal friction, and the need for safe, transparent, and verifiable frameworks to protect investors from scams.

- ICOs leaned entirely into financing speed, operating with low friction and no boundaries, but they triggered a massive wave of retail scams.

- IEOs shifted the screening burden back onto centralized exchanges, restoring a level of institutional trust but reintroducing centralized gatekeepers and listing monopolies.

- IDOs attempt to establish a middle ground within the DeFi world, deploying smart contracts, automated liquidity pools, whitelists, and Launchpad platforms to balance execution velocity with baseline risk filtering.

However, an IDO does not eliminate risk. It simply restructures it, shifting the exposure from a "completely unvetted market" into a framework defined by Launchpad screening criteria, immutable on-chain smart contract execution, and absolute personal investor responsibility.

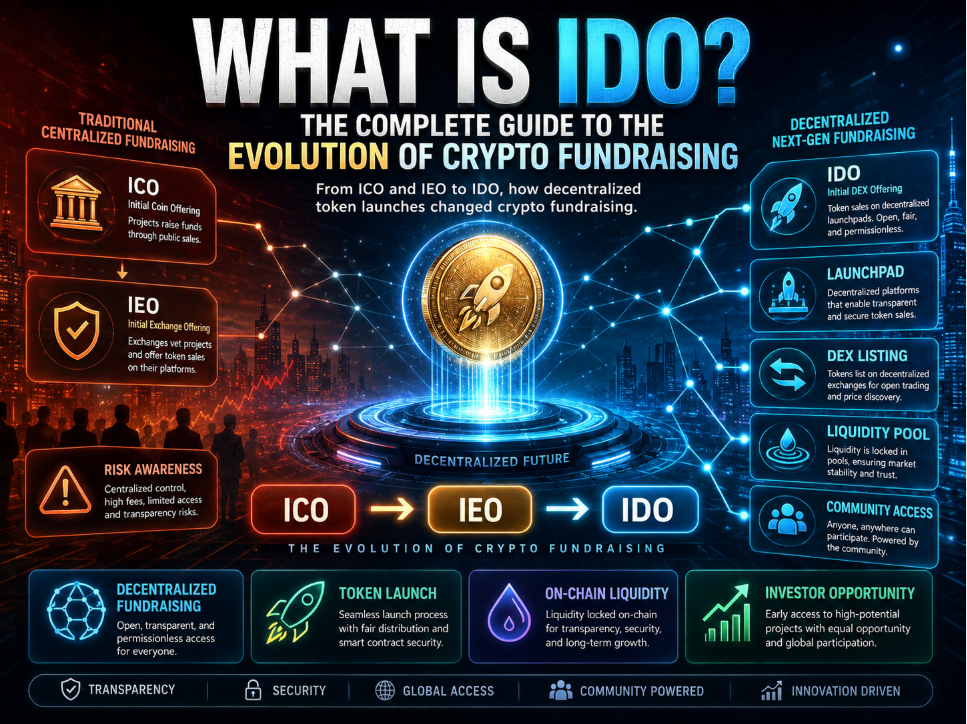

1.5 The Evolution from ICO to IEO and IDO

The structural shifts in crypto fundraising can be summarized as follows:

- ICO (Initial Coin Offering): Project teams sell tokens directly to global users from their own website interfaces. Pros: Extreme speed, total freedom. Cons: Rampant scams, severe regulatory vulnerabilities.

- IEO (Initial Exchange Offering): Centralized exchanges act as an intermediary, hosting the token sale for the project team. Pros: Platform screening and immediate liquidity/traffic. Cons: Extreme centralization, steep listing fees, highly restricted allocations for average retail users.

- IDO (Initial DEX Offering): Capital rounds are executed completely on-chain via decentralized exchanges or dedicated Launchpad protocols. Pros: Heightened decentralization, immediate automated liquidity pool provisioning, permissionless global baseline access. Cons: Complex user operation barriers, smart contract vulnerabilities, highly uneven project quality.

The IDO model is a structural iteration shaped by the lessons learned from the ICO and IEO eras that came before it.

Chapter 2: The ICO Era: Unchecked Growth and Structural Collapse

2.1 How ICO Mechanisms Operated

An ICO functions as an unmediated crowdfunding campaign. The project team follows a standard playbook:

- Release an introductory conceptual Whitepaper;

- Design the baseline tokenomics model structure;

- Broadcast a public crowdfunding smart contract or wallet address;

- Investors send capital contributions (such as BTC, ETH, or stablecoins) directly to the address;

- The project team accumulates the funds;

- The project team distributes their newly minted tokens back to the contributors' addresses;

- The founders promise to develop the product, secure exchange listings, and grow the network over time.

During the mania of 2017, a project team often needed little more than a PDF whitepaper, a basic website landing page, an active Telegram group, and a deposit address to accumulate millions of dollars within minutes. This friction-free model appeared highly efficient, but its main benefit was also its fatal flaw: raising capital was effortlessly easy, while holding teams accountable was practically impossible.

2.2 The Euphoria of the 2017 ICO Boom

The year 2017 marked the absolute peak of the ICO bubble, with billions of dollars pouring into token crowdfunding campaigns globally. For many retail investors, this was their first realization that early-stage token sales could yield returns that dramatically outpaced traditional venture investments.

A handful of these projects successfully built foundational web3 infrastructure that endures today:

- Ethereum

- Chainlink

- Filecoin

- Tezos

- EOS

- Bancor

- 0x

However, the vast majority of ICO-era projects eventually went dark, abandoned development, or collapsed below their issuance price. The systemic problem with ICOs was not a total absence of success stories; it was that those high-profile success stories were heavily romanticized, drawing a massive influx of low-quality projects, copycat codes, and outright fraudulent Ponzi schemes into the market.

2.3 Why Did the ICO Model Face a Systemic Collapse?

The death of the ICO model was driven by four clear structural flaws:

- Zero Entry Barriers Triggered Rampant Fraud: Because anyone could launch a token with a basic website and a copy-pasted whitepaper, malicious actors flooded the market to siphon away retail capital with no intention of building real products.

- Complete Lack of Post-Fund Oversight: Once a team secured millions in crowdsourced ETH, there were no legal frameworks or governance locks to force them to hit milestones. With no mandatory financial reporting or independent audits, investors had to rely entirely on the team's honesty.

- Extreme Information Asymmetry: Institutional insiders and early venture backers routinely secured massive token tranches at seed valuations that were a fraction of the public ICO price. Once the token hit centralized exchanges, these low-cost insiders used retail buyers as exit liquidity.

- The Rapid Encroachment of Global Regulation: As public token sales grew into multi-billion-dollar global phenomena, securities regulators intervened. Agencies like the U.S. SEC and global financial watchdogs issued stark warnings, fines, and absolute bans on unvetted public token offerings, cooling the market down.

2.4 The Howey Test: Why ICO Tokens Fell into the Securities Net

When evaluating digital assets, the United States Securities and Exchange Commission (SEC) relies heavily on the Howey Test. Under this legal framework, a transaction is classified as an investment contract (and thus a security) if it satisfies four clear conditions:

- It is an investment of money;

- It is made into a common enterprise;

- There is a reasonable expectation of profits;

- Those profits are derived primarily from the entrepreneurial or managerial efforts of others.

The marketing playbooks of most ICO campaigns explicitly matched these criteria: retail users contributed capital to buy a token with a clear expectation that the core engineering team would build a network, secure listings, drive demand, and pump the token's spot value. Consequently, a massive number of ICO projects faced severe legal vulnerabilities for executing unregistered securities offerings.

2.5 The Lasting Contributions of the ICO Era

Despite the collapse of the 2017 bubble, the ICO experiment left behind several critical innovations that shaped modern web3:

- It proved that global, borderless community crowdfunding was structurally viable;

- It gave retail participants unprecedented access to early-stage network protocols;

- It catalyzed the widespread adoption of the ERC-20 token standard;

- It laid the groundwork for innovations like DeFi, decentralized autonomous organizations (DAOs), and tokenomics engineering;

- It successfully funded several genuine, high-quality development teams who built actual infrastructure.

The core lesson of the ICO era was not that decentralized crowdfunding was an invalid idea, but that it could not survive without robust risk management, independent vetting, transparency, and consumer protections. This set the stage for the rise of the IDO.

Chapter 3: The IEO Era: Centralized Exchanges Take the Reins

3.1 The Structural Shift of the IEO Model

An IEO, or Initial Exchange Offering, introduced a clear structural change: instead of a project team selling tokens directly to the public from their own website, a top-tier Centralized Exchange (CEX) acts as the launch platform.

This configuration introduced a major layer of trust: the exchange became the primary gatekeeper. Retail participants reasoned that if a project cleared the compliance and listing due diligence of a top exchange, it possessed a higher layer of baseline legitimacy than a random website ICO. The exchange provides immediate access to its user base, massive trading traffic, marketing amplification, and a guaranteed liquid trading market immediately post-sale. The core value proposition of an IEO was simple: replace unverified project claims with the institutional reputation and balance sheet credit of an established exchange platform.

3.2 The Launchpad Allocation Blueprint (Binance Launchpad Model)

The execution flow pioneered by platforms like Binance Launchpad established a clear format for the IEO era:

- Users are required to accumulate and hold the exchange's native utility token (e.g., BNB) over a set observation period;

- The platform takes daily automated balance snapshots to calculate each user’s maximum eligibility cap;

- Users commit their utility tokens to a subscription pool during a specific window;

- An automated allocation engine distributes the new project tokens either through a lottery system or via a pro-rata subscription percentage;

- The designated exchange immediately opens live spot trading pairs for the token;

- All unspent or unallocated utility tokens are returned to the users' spot balances.

While this framework brought order and massive marketing traffic to token launches, it also introduced a clear barrier: retail users without massive holdings of the native exchange token could rarely secure meaningful allocations. The demand for hot tokens far outpaced supply, leaving average users with tiny allocations.

3.3 The Real-World Performance Metrics of IEOs

The IEO boom generated notable short-term wealth effects, with early projects like BitTorrent, Fetch.ai, and Matic Network (Polygon) capturing massive market attention and surging immediately post-listing.

However, over a long-term horizon, IEO returns proved highly uneven. While a few select tokens evolved into blue-chip assets, many others experienced brief initial pumps followed by long-term declines in volume and liquidity. The underlying reality remained unchanged: an IEO is still an early-stage token investment. An exchange’s screening process can filter out crude exit scams and absolute vaporware, but it cannot guarantee a project’s long-term product-market fit or business execution.

3.4 Three Structural Flaws of the IEO Model

- The Return of Centralized Gatekeepers: The IEO model solved the unvetted chaos of ICOs by giving complete control back to centralized exchange executives. The exchange holds absolute monopoly power over who gets listed, at what valuation, and under what timeline.

- Severe Retail Allocation Crowding: Because top-tier IEO campaigns attract millions of global participants, the allocation pools are diluted. Retail users who purchase volatile exchange utility tokens simply to participate frequently find their final token allocations so small that the returns fail to offset the spot price volatility of the underlying exchange token.

- Loss of Project Independence: Project teams must give up substantial control over their token economics, pricing structures, distribution logic, and market timelines to satisfy exchange requirements, often alongside paying steep listing fees and liquidity provisions.

3.5 Why the IEO Craze Gradually Cooled Down

By 2019 and 2020, the IEO mania began to lose steam due to several compounding trends:

- The initial post-listing pumps diminished, and a growing number of tokens began breaking below their public launch prices;

- The financial risk of holding volatile exchange utility tokens outpaced the diminishing yields of the launch allocations;

- The historic "DeFi Summer" of 2020 exploded, violently redirecting market attention, capital, and developer talent back onto decentralized blockchains;

- The meteoric rise of Automated Market Makers (AMMs) like Uniswap and SushiSwap proved that liquid trading markets could be launched permissionlessly without exchange approvals.

This set the stage for the rise of the IDO.

Chapter 4: What Is an IDO? Mechanics, Frameworks, and Execution Logic

4.1 Defining the Initial DEX Offering (IDO)

An IDO stands for Initial DEX Offering. Breaking down the components reveals its core architecture:

- Initial: The token is being offered to the public or an ecosystem community for the very first time.

- DEX (Decentralized Exchange): The entire asset distribution, capital collection, and post-launch trading market are managed natively via on-chain liquidity pools and smart contracts rather than a centralized system.

- Offering: The project sells a set allocation of its token supply to secure early development funding while bootstrapping its decentralized community.

Put simply: An IDO is a decentralized fundraising framework where a project issues and distributes its tokens directly on-chain via a DEX or a specialized Launchpad protocol, with automated liquidity pools opening for live trading immediately post-sale.

4.2 Automated Liquidity Pool Bootstrapping: Why IDOs Feature Instant Secondary Markets

One of the most important structural differences between an IDO and an ICO is the mechanism used to bootstrap trading liquidity. In the ICO era, after a token sale closed, investors faced long delays while the project team negotiated listings with centralized exchanges. If no exchange approved the token, it remained illiquid indefinitely.

An IDO solves this by utilizing smart contracts to automate liquidity creation on an AMM DEX immediately. The standard execution logic works as follows:

$\text{Capital Raised from Public Allocation} \longrightarrow \text{Automated Smart Contract Locking} \longrightarrow \text{DEX Liquidity Pool Generation (Token / Stablecoin)}$

The project team configures a launch smart contract that splits the incoming fundraising capital. A pre-set percentage of the raised funds (e.g., USDT, ETH, or BNB) is combined with a designated allocation of the project's new tokens and automatically deposited into a fresh DEX liquidity pool.

This mechanics design yields two immediate outcomes:

- Instant Market Access: The token transitions to a live, tradable asset the exact second the public allocation round concludes.

- Decentralized Price Discovery: The asset's spot rate adjusts continuously via the AMM's mathematical constant product formula ($x \cdot y = k$), driven entirely by live market demand.

However, this architecture introduces a clear risk: if the initial depth of the automated liquidity pool is too shallow, minor buy or sell orders will trigger massive price volatility, leaving the pool vulnerable to manipulation or sudden drainage.

4.3 The Step-by-Step Lifecycle of a Standard IDO

The lifecycle of a standard IDO can be broken down into seven clear phases:

[1. Project Warm-up] ➔ [2. Whitelist Action] ➔ [3. Validation & Tiering]

│

[6. Liquidity Injection] ➔ [5. Token Vesting] ➔ [4. Public Contribution]

│

[7. Live DEX Trading]

- Project Warm-up & Vetting: The project publishes its core whitepaper, codebases, tokenomics, roadmap milestones, and strategic audit certifications. The hosting Launchpad schedules the upcoming pool parameters and introduces the project to its user community.

- Whitelist Application Action: To filter out automated bots and coordinate allocations, users must complete specific on-chain and off-chain tasks: following social channels, verifying community profiles, completing identity checks (where mandated), and linking a Web3 wallet address.

- Validation & Tier Confirmation: The Launchpad protocol audits the applicants, applies its internal staking rules, and publishes the final list of whitelisted wallet addresses along with their allowed allocation capacities.

- The Public Contribution Window: The smart contract opens for deposits. Whitelisted users must send their contribution funds (e.g., USDC, USDT, ETH, or BNB) to the allocation contract within a strict time window (often spanning only a few hours).

- Token Vesting & Distribution: Once the funding pool closes, the smart contract calculates token distributions. Rather than releasing 100% of the tokens instantly, the contract often triggers a Vesting Schedule, unlocking a specific percentage at the Token Generation Event (TGE) and releasing the remainder linearly over a set number of months.

- Automated Liquidity Injection: The allocation smart contract automatically moves the designated liquidity-provisioning tokens into a DEX pool (e.g., Uniswap or PancakeSwap) and burns or locks the resulting Liquidity Provider (LP) tokens inside a time-lock contract to prevent rug pulls.

- Live DEX Trading Market: The pool opens for public trading. Anyone can buy or sell the token on the secondary market, and arbitrage bots step in to align prices across alternative venues.

4.4 Common IDO Pricing Models

IDOs deploy a variety of structural pricing designs to match different asset distribution strategies:

- Fixed-Price Model: Tokens are distributed at a static, unaltering price (e.g., 1 Token = 0.05 USDT). While highly predictable, hot offerings spark intense gas wars or instant sell-outs, while cold offerings risk failing to hit their funding soft caps.

- Dutch Auction Framework: The token price starts at an intentionally elevated ceiling and automatically decays lower over time according to a set mathematical formula. The auction closes once the market buying volume fully absorbs the total available allocation pool. This structure eliminates gas wars and limits bot manipulation, but it demands a higher layer of technical understanding from retail participants.

- Dynamic AMM Pricing: The token is launched directly into a public liquidity pool with zero fixed pre-sale rounds, allowing the immediate buying and selling volume to drive price discovery from minute one. This maximizes market efficiency, but it exposes retail users to extreme initial volatility and aggressive front-running by automated MEV arbitrage bots.

- Liquidity Bootstrapping Pools (LBPs): Championed by ecosystems like Balancer, LBPs use dynamically shifting token weights (e.g., starting at a 99:1 weight and gradually normalizing to 50:50) to create downward price pressure over time. This mechanism discourages front-running bots and whale concentration, allowing retail users to wait and buy in at a price point they deem fair.

4.5 Comparative Matrix: ICO vs. IEO vs. IDO

4.6 The Role of Smart Contracts in the IDO Process

In an IDO, trust is shifted from centralized exchange executives onto immutable blockchain code. Smart contracts autonomously manage almost every step of the launch lifecycle:

- Validating whitelisted wallet signatures;

- Enforcing individual maximum contribution limits;

- Restricting access to pre-sale allocation pools;

- Processing capital deposits securely;

- Calculating and executing linear token vesting schedules;

- Managing automated refund protection windows;

- Injecting liquidity into AMM trading pools;

- Locking liquidity provider (LP) tokens in secure time-lock vaults.

While this ensures transparency, it also means that any undiscovered exploit or logical flaw within the launch smart contracts can lead to a complete drainage of user deposits, distribution errors, or malicious developer manipulation. Sophisticated investors must verify whether an IDO's core contracts are open-source, fully audited by reputable firms, and governed by multi-signature setups with explicit time-locks.

Chapter 5: The IDO Launchpad Ecosystem: Strategic Vetting and Platform Mechanics

5.1 Why the Market Mandates Dedicated Launchpad Intermediaries

Technically, any development team can deploy a smart contract, mint a token, and inject a liquidity pool directly into Uniswap or PancakeSwap without an intermediary. However, skipping a structured launch framework introduces severe execution hurdles:

- A complete lack of built-in marketing traffic and user visibility;

- No independent due diligence or third-party code verification;

- No built-in mechanism to distribute whitelists or manage token sybil attacks;

- High vulnerability to sniping bots that instant-drain initial pool liquidity;

- Low community confidence, which often causes investors to pass on the project;

- The high risk of unvetted tokens turning out to be rug pulls or honeypots.

Launchpads address these issues by acting as structured incubators. For development teams, a Launchpad provides immediate access to a vetted retail community, marketing amplification, and reliable smart contract deployment toolsets. For retail investors, a reputable Launchpad offers baseline project screening, transparent allocation mechanics, and an organized gateway to participate in early rounds.

5.2 Deep-Dive Profiling of Elite IDO Launchpads

Polkastarter

Polkastarter stands as one of the most established platforms in the cross-chain IDO space. It pioneered decentralized fundraising via cross-chain token pools, allowing projects to raise capital seamlessly across networks like Ethereum, BNB Chain, and Polygon. To secure allocation access, users must hold or stake its native token (POLS) to generate "POLS Power," which unlocks lottery tickets for whitelisting slots.

DAO Maker

DAO Maker pioneered the Strong Holder Offering (SHO) framework, an allocation methodology engineered to reward long-term community members rather than short-term speculators. Its platform relies on a sophisticated scoring system that monitors a user's on-chain history, asset holding periods, and staking volumes of its native token (DAO) to determine allocation access. It also features protection frameworks that offer partial user refunds if a launched token performs poorly post-listing.

Seedify

Seedify has carved out a highly successful niche by focusing exclusively on the GameFi, Metaverse, and play-to-earn Web3 gaming sectors. It utilizes a strict, multi-tiered staking model driven by its native token (SFUND). By specializing in Web3 gaming infrastructure, Seedify has built a dedicated, highly aligned community of gaming enthusiasts, making it a go-to launch platform for developers in that vertical.

Other notable platforms in the ecosystem include Poolz, BSCPad, TrustPad, Red Kite, and PAID Ignition. However, disciplined investors should look beyond historical brand prominence and evaluate live data points: real-time asset survival rates, current return on investment (ROI) metrics, and the active liquidity profiles of recently launched projects.

5.3 Explaining the Launchpad Monetization Blueprint

Investors must recognize that Launchpads are commercial businesses whose financial interests do not always perfectly align with retail participants. Launchpads typically generate revenue through multiple streams:

- Charging upfront platform listing fees to project teams;

- Retaining a percentage of the newly minted project tokens;

- Requiring users to buy and lock up their platform tokens, which drives up demand and utility for the launchpad’s native token;

- Taking a percentage fee from the total capital raised during the public funding round;

- Providing premium advisory, marketing, and market-making consulting packages to projects for an ongoing retainer.

A launchpad’s primary commercial goal is to maintain a packed launch pipeline, maximize user participation, and drive up the spot value of its own native staking token. Retail investors, on the other hand, care about strict project quality, conservative launch valuations, fair vesting terms, and long-term token survival. Therefore, do not judge a platform simply by the number of projects it launches; evaluate how well those projects perform 6 to 12 months post-launch.

5.4 The Tiered Staking Architecture: The Cost of Securing Allocations

To allocate fundraising pools systematically, almost all elite Launchpads employ a rigid, tiered subscription model based on token holdings:

[Tier 1: Entry Level] ➔ Hold 1,000 Platform Tokens ➔ Low Lottery Ticket Probability [Tier 2: Mid-Tier] ➔ Hold 5,000 Platform Tokens ➔ Expanded Pool Weight Allocation [Tier 3: Executive] ➔ Hold 20,000 Platform Tokens ➔ Guaranteed Allocation Capacity

While this design mechanics drives buying demand for the launchpad's native asset, it introduces clear headwinds for retail participants:

- High Financial Barriers to Entry: Retail users are forced to risk thousands of dollars purchasing a volatile launchpad token simply to clear the tier entry threshold.

- Exposure to Platform Token Depreciation: The capital depreciation risk of holding the launchpad token can easily eclipse the trading profits generated from your IDO token allocations.

- Whale Concentration: Guaranteed allocations are heavily skewed toward high-tier whale stakers, leaving retail participants with highly diluted, negligible allocation limits.

5.5 Six Indicators to Evaluate a Launchpad’s Legitimacy

Before locking your capital into a launchpad ecosystem, evaluate it across six clear operational metrics:

- Long-Term Project Survival Rate: What percentage of their historically incubated projects are actively building and delivering on their roadmaps today? Are they real products, or were they short-term hype plays that trended to zero?

- Historical Return on Investment (ROI): Analyze the platform’s average All-Time High (ATH) ROI alongside its Current ROI across all launched projects to spot down-cycles.

- Transparency of Project Vetting Standards: Does the platform publicly disclose its internal auditing criteria? Do they perform deep background verification on code audits, team background tracking, and tokenomics sanity checks?

- Token Distribution Transparency: Does the platform clearly disclose and contrast the public IDO pricing against the seed round costs, institutional private round valuations, and insider vesting terms?

- Contract Security and User Protection History: Has the launchpad infrastructure ever suffered a smart contract exploit? Do they deploy automated consumer safeguard mechanisms, such as mandatory conditional refund windows?

- Organic Community Health: Is the launchpad’s social media community driven by genuine, long-term investors asking product questions? Or is it flooded with automated bot accounts and airdrop hunters chasing hype?

5.6 Practical Toolsets to Audit Historical Launchpad Performance

To bypass marketing claims and analyze real protocol performance, track live data across these web3 analytics platforms:

- CryptoRank: Provides comprehensive dashboards tracking historical launchpad performance, offering deep insights into average ATH ROI, current token yields, listing drawdowns, and complete historical funding data.

- ICO Drops: A highly reliable historical database tracking ongoing, upcoming, and concluded token allocation rounds across multiple launch platforms.

- DefiLlama / TokenUnlocks: Essential for mapping real-time Total Value Locked (TVL) metrics, verifying on-chain pool depth, and identifying upcoming token vesting cliffs that could trigger market sell pressure.

- Etherscan / BscScan / Solscan: The ultimate on-chain source of truth. Use blockchain explorers to audit the code architecture of the IDO distribution contracts, verify the wallet transfers of core founders, and track real-time token holder distribution metrics.

Chapter 6: The Retail Participant Blueprint—Navigating an IDO from Discovery to Exit

6.1 Finding Early IDO Opportunities Before Listing

To locate upcoming IDO allocation rounds before registration windows close, monitor these primary information flows:

- Launchpad Dashboards: Check the "Upcoming Offerings" schedules on verified platforms like Polkastarter or DAO Maker regularly.

- Crypto Aggregators: Use the dedicated token launch calendars hosted on CryptoRank, ICO Drops, CoinGecko, and CoinMarketCap.

- Ecosystem Social Feeds: Monitor curated developer updates and alpha disclosure threads on Twitter/X, Discord, and Telegram.

- DeFi Analytics Boards: Track the "New Tokens" and "Trending Pools" discovery tabs inside DefiLlama and Dune Analytics to identify early project momentum.

Operational Reality: The earlier you locate an unlaunched project, the higher the underlying execution risk usually is. Finding an unvetted project early does not automatically mean it is a safe investment opportunity.

6.2 The Comprehensive IDO Project Due Diligence Checklist

Before committing capital to any IDO allocation round, ensure you can answer these ten foundational due diligence questions:

- Can the team's identity and professional history be independently verified? While anonymous teams are a staple of web3, they introduce a significantly higher layer of risk and make accountability practically impossible if a rug pull occurs.

- What real-world problem does the project solve? Is the dApp delivering a highly demanded, sticky utility solution? Or is it simply a copy-pasted codebase chasing a short-term market narrative?

- Is there a functional MVP (Minimum Viable Product)? Projects launching with an active testnet or a functional beta app are significantly safer than projects raising millions based solely on a PDF whitepaper and conceptual mockups.

- What programmatically drives the utility of the token? Is the token a core functional fuel for network gas fees, mandatory staking security, or cash-flow revenue capture? Or is it a useless meme asset built solely for speculative trading?

- Are the launch valuation metrics sane? Compare the project's public IDO Market Cap and Fully Diluted Valuation (FDV) against established, live competitors in the same sector. If a project launches at an inflated FDV with minimal initial circulating supply, the valuation is unsustainable.

- What is the exact cost discrepancy across early funding rounds? If institutional seed and private venture rounds secured tokens at a 90% discount relative to the public IDO price, retail participants face massive structural sell pressure the moment those insider tokens unlock.

- Is the token vesting schedule fair and sustainable? Does the vesting architecture enforce extended, multi-year linear cliff intervals for team members, advisors, and early venture funds? Or are insiders allowed to dump massive allocations onto the market early on?

- What is the historical performance profile of the host Launchpad? Does the platform have a track record of launching successful, long-term projects, or does it primarily pump out low-tier short-term hype plays?

- Has the codebase passed a rigorous third-party smart contract audit? While a code audit from a firm like CertiK or OpenZeppelin does not guarantee absolute security, a complete lack of a professional audit is an immediate red flag.

- What is my explicit exit and capital risk strategy? Have you defined a clear framework for your allocation? Will you sell 100% of your unlocked tokens at the TGE opening candle, take profits in tranches as milestones are hit, or hold for long-term growth? If the token breaks below its issuance price, what is your maximum risk cut-off point?

6.3 Navigating the Whitelist Application Process Safely

Securing a whitelisted allocation slot typically requires completing a structured sequence of actions on the launchpad interface:

- Connect your Web3 wallet to the verified launchpad dashboard and complete any required identity checks (KYC);

- Link your active social profiles (Twitter/X, Discord, Telegram) to verify your identity;

- Complete designated community onboarding actions: following official project channels, joining server communities, and sharing verified announcement posts;

- If the platform operates a tiered model, stake the required volume of native launchpad tokens inside the governance contract to lock in your eligibility;

- Complete any required educational project quizzes or testnet interactions;

- Submit your final cryptographic signature via your wallet to lock in your application entry, and check the portal announcements for the final whitelisting selections.

Critical Security Warning: Any website or pop-up interface that requests you to input your private key or seed phrase to verify a whitelisting slot is an absolute scam. Reputable Launchpads interact entirely through standard on-chain wallet approvals and off-chain cryptographic signatures. Ignore any unsolicited direct messages on Telegram or Discord claiming you have won a special allocation slot—these are phishing attacks designed to drain your wallet assets.

6.4 Preparing Your Web3 Wallet for Capital Contribution

Once your wallet address clears the whitelisting lottery hurdles, ensure your address is loaded with the required contribution assets and gas fees well ahead of the deposit window opening.

- Contribution Stablecoins: Ensure your wallet holds the exact type of stablecoin or asset requested by the project contract (typically USDT, USDC, ETH, BNB, or SOL).

- Native Network Gas Reserves: You must hold a baseline balance of the network’s native token to fund transaction gas fees.

Before the contribution window opens, verify that your wallet is connected to the correct blockchain network, that you are using the verified wallet address, and that you have sufficient gas tokens to cover network congestion spikes.

6.5 Tactical Execution on the Public Contribution Day

The actual day of the public allocation deposit is often a fast-moving environment where minor mistakes can cause you to miss your allocation. Follow these operational guidelines:

- Navigate to the launchpad interface early and manually verify the exact character string of the URL to ensure you are not on a phishing site;

- Connect your Web3 wallet, verify your network status, and execute any required token allowance approvals well ahead of the open candle;

- Monitor the interface countdown clock closely. In a First-Come, First-Served (FCFS) model, allocation pools can sell out completely within seconds;

- If the network experiences severe traffic congestion, adjust your wallet's gas price settings manually to "High" or "Aggressive" to ensure your deposit transaction processes ahead of the crowd;

- Avoid connecting to public, unencrypted Wi-Fi networks during the contribution window, and do not click on sudden troubleshooting links shared in community chat groups.

6.6 Post-Launch Exit Strategies: Instant TGE Arbitrage vs. Long-Term Staking

The second your IDO tokens are distributed to your wallet and the DEX liquidity pool goes live, you must execute your pre-planned strategy without letting market emotions take over:

- The Instant TGE Market Sell-Out Strategy: This approach focuses on selling 100% of your initial unlocked token allocation the exact second trading opens on the DEX. This is ideal for short-term swing traders looking to lock in rapid pre-sale profits and immediately eliminate their downside capital risk. The main downside is missing out on any sustained, long-term upward trends if the project experiences a massive post-launch run.

- The Balanced Tranche De-Risking Strategy: This method balances short-term profits with long-term upside. You sell a set portion (e.g., 50%) of your initial unlocked tokens on the opening day to fully recoup your baseline seed investment capital. Once your initial capital risk is entirely cleared, you retain the remaining tokens to take advantage of future milestones, selling in staggered tranches as the team delivers on its roadmap.

- The Conviction Long-Term Holding Strategy: Under this approach, you retain 100% of your allocated tokens and actively stake them to generate additional ecosystem rewards, run network validation nodes, or participate in DAO governance. This strategy is only rational for investors who have deep conviction in the project's long-term utility. It leaves you exposed to token vesting dilutes, secondary market drawdowns, and the risk of the project failing completely over time.

Chapter 7: The Centralized Alternative—Navigating New Token Offerings on HIBT

7.1 Why the Technical Overhead of On-Chain IDOs Barriers Retail Beginners

For absolute beginners, participating in a native on-chain IDO presents a steep learning curve. The process requires a solid grasp of Web3 wallet mechanics, seed phrase security, gas fee calculations, cross-chain bridging, smart contract interactions, token allowance risks, slippage settings, AMM liquidity dynamics, and identifying phishing sites. A single mistyped character or an accidental signature approval can lead to an immediate and irreversible loss of capital. Consequently, centralized platform subscription events offer a far safer, more accessible entry point for newcomers looking to gain exposure to early-stage tokens.

7.2 Understanding the Mechanics of Centralized New Token Offerings

When a premier centralized trading venue like HIBT hosts an early-stage launch event—whether through an integrated Launchpad, an active Launchpool, or an exclusive pre-listing subscription drive—the platform takes over the complex technical heavy lifting. Users simply need to navigate to the platform interface and analyze the explicit event parameters:

- The core project background, utility thesis, and audit status;

- The precise schedule for subscription openings, allocation calculations, and live spot trading listings;

- The baseline account eligibility mandates and required identity verification (KYC) tiers;

- The supported crypto assets allowed to be committed to the subscription pools (typically USDT or platform utility tokens);

- The maximum allocation cap allowed per individual participant to prevent whale manipulation;

- The exact formulas used to calculate allocations, fund freezing rules, and token distribution timelines.

Disciplined Market Reality: While a centralized platform like HIBT performs baseline operational due diligence, project vetting, and structural event design to protect users from crude scams, every early-stage token launch still carries severe market risks. Tokens can still drop below their initial launch price, suffer from extreme volatility, or experience thin liquidity post-listing. Investors must analyze the live event pages and project disclosures directly before risking capital.

7.3 Step-by-Step Guide to Participating in a Token Launch on HIBT

To participate in a token launch offering on HIBT, execute the following operational steps:

- Access the Official Platform: Log into your verified account via the official HIBT mobile application or secure web portal, avoiding any external links from third-party messages to ensure you are on the legitimate platform.

- Complete Verification Milestones: Ensure your account has cleared the mandatory KYC identity verification parameters required to unlock early-stage token sale features.

- Navigate to the Launch Hub: Open the "Launchpad," "Launchpool," or "Subscription Event Center" portal via the primary navigation interface.

- Audit the Project Metrics: Select the upcoming token event and carefully evaluate the project introduction, minimum subscription thresholds, event timelines, and risk parameters.

- Verify Your Regional Eligibility: Review the event terms to ensure your jurisdiction is not restricted from participating in that specific asset distribution round.

- Fund Your Subscription Wallet: Deposit or transfer the necessary commitment assets (such as USDT) into your designated spot account well ahead of the subscription window opening.

- Commit Your Assets: Enter your desired subscription size within the allowed limits during the active subscription window, and confirm the temporary freezing of those funds.

- Allocation Settlement Phase: The platform's automated engine processes all entries, calculates your pro-rata allocation based on total pool contributions, deducts the corresponding amount from your frozen funds, and unlocks the remaining capital back to your account.

- Inspect Your Token Balances: Once distribution completes, review your spot account balance to verify your new tokens have arrived safely ahead of the market opening.

- Execute Your Trading Strategy: Formulate your explicit sell or hold plan well before the live spot trading pairs open to ensure you execute your strategy objectively amidst fast market moves.

7.4 Comparative Analysis: On-Chain IDOs vs. Centralized Exchange Offerings

Centralized launch events eliminate complex technical hurdles and gas management issues for users, but they require you to operate within the exchange's hosted ecosystem. On-chain IDOs grant total permissionless autonomy but demand a high degree of personal security mastery.

7.5 How to Evaluate a Centralized Platform's Historical Launch Record

To evaluate the historical track record and quality of a platform’s token offerings, analyze these key metrics:

- The total volume of projects successfully incubated and listed over a rolling 12-month window;

- The average performance multiplier on day-one trading relative to the launch price;

- The mid-term spot price stability of tokens 30, 90, and 180 days post-listing to identify rapid pump-and-dump dynamics;

- The percentage of launched assets that maintain healthy trading volumes and active development updates;

- The overall execution stability of the platform's order matching engines during high-traffic opening minutes;

- The clarity, precision, and transparency of the platform's distribution rules and announcement timelines.

Always baseline your analysis on average historical performance across all launches rather than focusing solely on a few exceptional outliers that generated massive returns.

7.6 Capital Allocation and Risk Rules for Early-Stage Tokens

When trading newly issued tokens, maintaining disciplined capital management is your primary defense against sudden losses. Follow these fundamental rules:

- Enforce Strict Allocation Caps: Never deploy more than 1% to 5% of your total liquid investment capital into a single early-stage asset.

- Invest Only Discretionary Funds: Never risk essential capital needed for rent, living costs, or emergency reserves.

- Avoid Debt-Fueled Trading: Never leverage your positions using loans, margin, or credit cards to chase token launches.

- Keep Position Sizes Stable: Do not let a single successful trade tempt you into risking a larger portion of your portfolio on the next launch.

- Diversify Across Sectors: Avoid crowding your portfolio into a single hot vertical (e.g., allocating all your capital to AI tokens or Layer-2 memes).

- Do Not Chase Opening Spikes: Avoid FOMO-buying a token on the public spot market during the highly volatile initial opening minutes, as you risk buying at a localized top.

- Pre-Set Your Exit Rules: Always write down your explicit profit targets and risk thresholds before trading begins to prevent emotional decision-making.

Chapter 8: The IDO Risk Landscape—Why the Vast Majority of Early Projects Fail

8.1 The Reality of Post-IDO Project Survival Rates

The launch phase of an IDO project is frequently characterized by extreme excitement: social feeds are flooded with promotions, community channels experience explosive growth, and day-one token prices experience wild upward swings.

However, once the initial marketing buzz fades over a 6-to-12-month horizon, a pattern often emerges across the long-tail altcoin market:

- Project development velocity stalls, and official code commits go dark;

- Core founders withdraw from public community channels and stop updates;

- The asset's daily trading volume dries up completely on secondary markets;

- Token prices decline steadily, often dropping 90% or more below their all-time highs;

- Project roadmaps fail to deliver actual functional dApps or user adoption;

- The underlying DEX liquidity pools thin out, preventing investors from exiting size positions without triggering massive slippage.

The true gauge of an IDO investment is not how high the token spikes during its opening minute, but whether the project team possesses the operational capacity and resources to survive a multi-year market cycle.

8.2 Rug Pull Blueprints: Identifying Five On-Chain Red Flags

A rug pull occurs when developers abandon a project and maliciously steal investor capital, either by draining liquidity pools, exploiting contract backdoors, or dumping their team token allocations. Watch for these five warning signs:

[1. Anonymous Team] ➔ [2. Infinite Mint Rights] ➔ [3. Unlocked Liquidity Pools]

│

[5. Bot-Flooded Socials] ➔ [4. Vague Code/No MVP] ◄────────┘

- Complete Team Anonymity with No Track Record: The core founders operate behind unverified pseudonyms and lack a traceable professional history within the web3 or tech sectors.

- Infinite Mint Rights Built into the Contract: The token smart contract contains hidden functions or un-renounced owner privileges that allow developers to mint unlimited new tokens at will.

- Unlocked Liquidity Provider (LP) Tokens: The project team claims liquidity is secured, but an inspection of the blockchain explorer reveals that the LP tokens are held in a standard developer wallet rather than being locked inside a verifiable time-locked smart contract.

- Vague, Conceptual Whitepapers with No Working Code: The project's documentation relies heavily on buzzwords and lacks clear technical architecture, detailed smart contract code, or a working MVP.

- Bot-Flooded Social Channels: The project's social communities boast hundreds of thousands of members, but actual discussions consist entirely of generic, automated hype messages, while genuine technical questions are deleted by moderators.

If a project triggers multiple flags across this matrix, pass on the allocation.

8.3 The Vesting Unlock Death Spiral

To manufacture an artificial pump at launch, many projects keep their initial circulating token supply low. While this makes it easy for early buying volume to push the price higher, it sets up a structural challenge as subsequent vesting cliffs arrive.

When seed investors, institutional venture capital funds, marketing advisors, and core team members hit their monthly unlock milestones, a massive volume of low-cost tokens floods the liquid market. If the project fails to generate organic demand to absorb this expanding supply, the asset can quickly enter a classic death spiral:

$\text{Vesting Cliff Hits} \rightarrow \text{Insiders Dump Cheap Tokens} \rightarrow \text{Spot Price Plunges} \rightarrow \text{Community Panics} \rightarrow \text{Liquidity Dries Up} \rightarrow \text{Further Token Collapse}$

Before participating in an IDO round, closely analyze the Vesting Schedule. Do not look only at the public launch price; evaluate the exact entry cost of the earliest seed round participants. If early insiders bought in at a 95% discount relative to your IDO entry price, they remain highly profitable even if the token crashes 80% post-listing, giving them a strong financial incentive to sell immediately upon unlock.

8.4 The Illiquidity Trap

Many newly issued tokens suffer from a lack of deep secondary market liquidity. While a project's price chart might show an impressive percentage gain on low volume, retail holders often face severe friction when attempting to exit their positions:

- The automated liquidity pool depth on the DEX is shallow;

- Executing a market sell order triggers massive price slippage;

- The order book lacks sufficient buying depth to absorb larger size sales;

- A single large holder exiting can cause the spot price to crash instantly;

- The developers retain the technical ability to pull the underlying liquidity pool at any moment;

- The token contract contains malicious "honeypot" code functions that allow users to buy but completely block them from selling.

Always evaluate an asset's real-time Liquidity Depth and 24-hour trading volume rather than focusing solely on its nominal price action.

8.5 Institutional vs. Retail Information Asymmetry

The structural design of early-stage token fundraising is heavily skewed against retail participants. Before a project ever reaches a public IDO Launchpad platform, it has typically completed multiple private financing rounds:

$\text{Seed Round (Insiders)} \rightarrow \text{Private Round (VC Funds)} \rightarrow \text{Strategic Round (Partners)} \rightarrow \text{KOL Round (Promoters)} \rightarrow \text{Public IDO (Retail Group)}$

Each preceding round secures tokens at a significantly lower cost basis than the public IDO tier. If a project's token valuation is inflated to satisfy institutional exit targets, retail participants are essentially acting as late-stage exit liquidity for early venture backers and promotional influencers who are locked into near-zero cost structures.

8.6 The Hidden Opportunity Costs of Whitelist Hunting

Many retail participants spend hours grinding out whitelisting tasks: tracking social channels, joining server communities, referring friends, completing quizzes, and completing KYC verifications.

Before committing your time, perform a realistic calculation of your true opportunity costs:

- The value of the hours spent completing promotional tasks;

- Out-of-pocket transaction gas costs spent registering addresses on-chain;

- The capital depreciation risk of buying and holding volatile launchpad tokens to clear tier mandates;

- The privacy risk of exposing your sensitive identity documentation to unverified third-party KYC platforms;

- The low mathematical probability of actually winning a whitelisted slot out of tens of thousands of global applicants;

- The tiny individual allocation size (often capped at just $50 to $100) awarded to winning retail accounts;

- The high probability of the token breaking below its public launch price once secondary trading opens.

Often, the structural overhead and risk exposure of hunting for retail whitelists far outweigh the actual financial yields generated from the tiny token allocations you receive.

8.7 Smart Contract Security Risks

Because IDO crowdfunding campaigns interact entirely through smart contracts, your capital is exposed to various technical risk vectors:

- Critical vulnerabilities inside the contribution logic that allow hackers to drain public deposits;

- System logical bugs that cause user refund claims to fail or freeze permanently;

- Code compilation errors that result in the wrong volume of tokens being distributed;

- Intentional developer backdoors that allow creators to alter contract parameters mid-sale;

- Flawed liquidity-locking contract structures that allow developers to pull LP tokens early;

- Discovered zero-day exploits within the underlying blockchain network or host DEX platform.

An independent code audit can significantly reduce these technical risks, but it can never eliminate them entirely. Software code is always subject to undiscovered exploits.

Chapter 9: The Post-IDO Evolution—Fundraising Paradigms (2024–2026)

9.1 Liquidity Bootstrapping Pools (LBPs)

To address the gas wars and bot front-running issues common in fixed-price IDOs, the web3 space has increasingly adopted Liquidity Bootstrapping Pools (LBPs), typically hosted within ecosystems like Balancer. An LBP utilizes a dynamic variable-weight smart contract design to coordinate token launches.

The pool launches with an asymmetric asset weight (e.g., 95% project tokens to 5% collateral stablecoins), driving the initial price artificially high. Over a multi-day window, the smart contract automatically adjusts the pool weights toward a standard 50:50 ratio according to a linear mathematical formula. This mechanism creates consistent downward price pressure over time. If buyers rush in too quickly, the price moves up, but if buying pressure pauses, the contract weights push the price lower. This design eliminates gas wars and front-running bots, allowing retail users to wait and buy in at a price point they deem fair.

9.2 Fair Launch Movements

The Fair Launch movement emerged as a direct community pushback against the institutional venture capital models that dominated early token sales. A true Fair Launch enforces a clear structural mandate: zero pre-sale allocations, zero institutional seed funding rounds, zero low-cost allocations for insiders, and zero advisor token handouts. Every single participant—from the core founding engineers to retail buyers—enters the token market from the exact same starting point at the same public price.

While highly equitable in theory, practical execution still faces hurdles: early information asymmetry allows developers to front-run deployments, highly sophisticated technical users can optimize their node setups to sweep initial supplies, and well-funded whales can still leverage their deep capital reserves to capture a dominant percentage of the circulating token supply immediately upon launch.

9.3 NFT-Gated Access Allocation Frameworks

A growing number of projects require users to hold a specific utility NFT to clear the whitelisting hurdles for their IDO token allocations. This framework serves multiple structural purposes:

- Filtering out automated bot networks and sybil airdrop farms;

- Setting a distinct financial barrier to entry to verify community alignment;

- Giving real utility and floor value back to the project’s digital collections;

- Cultivating a highly committed core community of long-term holders.

However, this framework introduces parallel risks for retail participants: the cost of purchasing the required entry NFT can be bid up to unsustainably high levels by speculators, forcing you to take on capital loss risk on the NFT itself before you ever secure your token allocation. If the subsequent token distribution cap is small, your trading profits may fail to offset the price depreciation of the underlying entry NFT.

9.4 Points Systems and Token Generation Events (TGE)

The current token launch landscape relies heavily on the Points-to-Airdrop model over traditional public pre-sales. Under this framework, projects bypass upfront crowdfunding rounds and instead reward users with off-chain loyalty points for actively interacting with their protocol:

$\text{User Interacts with Protocol Suite} \rightarrow \text{System Logs Accumulating Points} \rightarrow \text{TGE Mapping Event} \rightarrow \text{Direct Token Airdrop Distribution}$

Users accumulate points by completing various on-chain actions: providing liquidity to automated market maker pools, executing trading volumes, completing daily tasks, and inviting network referrals. Once the project hits its TGE milestone, these accumulated points are mapped according to a set formula and converted into a direct token airdrop.

The clear benefit of this model is that users contribute liquidity and usage rather than spending out-of-pocket capital to buy pre-sale tokens. The downside is that the distribution formulas are completely opaque, points programs are often extended indefinitely to farm user activity, and massive dilution from professional sybil farms can leave retail participants with negligible real token allocations at the final distribution.

9.5 Security Token Offerings (STOs): Regulated Digital Issuance

An STO, or Security Token Offering, represents the intersection of blockchain technology with traditional securities law. Unlike permissionless ICOs or IDOs, an STO operates strictly within established state regulatory frameworks. The distributed tokens are legally classified as securities, explicitly representing real-world asset rights: corporate equity shares, fractional debt notes, dividend yield rights, or real estate fund ownership.

While STOs offer institutional-grade legal compliance, transparency, and consumer protections, they sacrifice the permissionless, fluid nature of DeFi. Launching an STO requires navigating slow regulatory reviews, paying steep compliance and legal costs, and restricting access strictly to accredited, KYC-verified investors, making them look far more like traditional capital markets than open-source web3 projects.

9.6 Fundraising Trends in AI + Crypto Projects (2025–2026)

The current web3 landscape is seeing an explosion of hybrid AI + Crypto protocols. These projects deploy a variety of fundraising models to bootstrap their decentralized networks:

- Hosting public node allocation sales where users purchase licenses to run decentralized processing clients;

- Issuing specialized compute power vouchers or data contribution tokens;

- Utilizing loyalty points programs to reward users for cleaning and providing machine learning training datasets;

- Launching micro-allocation public rounds via specialized AI infrastructure Launchpads;

- Restricting early token pools to holders of utility NFTs that grant developer access to their AI agents.

Investors must maintain a high degree of skepticism when evaluating this sector. The "AI narrative" is frequently copy-pasted onto low-quality roadmaps that lack actual functional machine learning architectures, real computing infrastructures, or sustainable business models simply to exploit current market hype.

Chapter 10: Legal Realities, Tax Treatments, and Global Regulatory Standards

10.1 Does Participating in an IDO Allocation Trigger a Taxable Event?

Tax treatment varies significantly across international jurisdictions. Generally, the simple act of using stablecoins (such as USDT or USDC) to participate in a public IDO allocation contract is legally viewed as a asset-for-asset exchange. If you use an asset like ETH to purchase the new token, you will immediately trigger a capital gains tax realization event on the ETH you contributed based on its fair market value at that exact second.

Furthermore, receiving your tokens at a TGE or claiming your unlocked tranches along a linear vesting schedule can trigger immediate income or wealth tax liabilities depending on your local regulations.

To ensure accurate tax reporting, maintain a detailed ledger of every step of your allocation:

- The exact timestamp and fiat value of the assets contributed to the pool;

- The gas fees consumed to execute the contract calls;

- The precise market value of the tokens at the exact second they are unlocked and claimed;

- The timestamps, values, and transaction hash strings for your subsequent secondary market sales.

10.2 Global Regulatory Approaches to On-Chain Public Allocations

- United States: The U.S. SEC maintains a strict regulatory approach toward public token sales, consistently applying the Howey Test framework to determine securities classifications. The agency actively pursues civil enforcement actions against project teams that distribute un-exempted tokens to public retail markets without formal registration.

- Hong Kong: The Securities and Futures Commission (SFC) has established a structured licensing regime for Virtual Asset Trading Platforms (VATPs). Protocols looking to distribute tokens or operate trading portals within the region must adhere to strict consumer protection compliance standards and clear asset qualification vetting pipelines.

- Singapore: The Monetary Authority of Singapore (MA) oversees digital token activities under its Payment Services Act framework. While the jurisdiction welcomes web3 innovation, it enforces strict compliance guidelines regarding Anti-Money Laundering (AML) controls and routinely issues consumer warnings highlighting the high volatility of early-stage crypto assets.

- European Union: The comprehensive Markets in Crypto-Assets (MiCA) regulation establishes a uniform compliance standard across all EU member states. MiCA imposes strict transparency mandates, requiring token issuers to publish regulated crypto-asset whitepapers, assume legal liability for accuracy, and maintain audited structural disclosures.

10.3 Why IDO Platforms Enforce Geoblocking Restrictions

When navigating IDO launchpads, you will frequently run into strict geoblocking pop-ups that prevent IP addresses from the United States, Mainlnd China, and various alternative jurisdictions from participating in allocation pools. Platforms deploy these restrictions for clear compliance reasons:

- Avoiding the risk of civil enforcement actions or unregistered securities litigation from the U.S. SEC;

- Complying with strict domestic bans regarding token crowdfunding and speculative crypto asset trading within Mainlnd China;

- Minimizing the steep operational overhead of implementing multi-jurisdictional compliance and corporate tax reporting;

- Shielding the development team from cross-border legal liabilities based on advice from their compliance counsels.

Consequently, reputable IDO Launchpads require mandatory KYC verifications and automatically block addresses originating from restricted regions.

10.4 The Compliance and Operational Risks of Using a VPN to Bypass Geoblocks

Many retail users attempt to deploy Virtual Private Networks (VPNs) to mask their physical locations and bypass launchpad geoblocks. This introduces significant risks:

- Immediate Allocation Forfeiture: If the launchpad’s security systems identify a blacklisted IP address or flag a proxy network, the platform retains the right to instantly cancel your whitelisting slot, freeze your committed capital, or block you from claiming your tokens, with no avenue for legal recourse.

- Violating Domestic Laws: Bypassing platform controls to participate in un-exempted token rounds can place you in direct violation of your local financial regulations, exposing you to severe potential legal liabilities and tax penalties.

Retail investors should never deploy VPNs to force entry into restricted token allocation pools.

10.5 Building a Digital Asset Record-Keeping System

To track your allocations for future tax reporting and strategy analysis, maintain a structured ledger using spreadsheet software or dedicated crypto tax tools:

Supplement your manual records with specialized tools: use platform data exporters from crypto tax tools like Koinly or TokenTax, track your multi-chain portfolio history via dashboard tools like DeBank, and archive screenshots of every contract contribution receipt and TxID hash string.

Chapter 11: Twelve Common Beginner IDO Mistakes and Risk Mitigation Strategies

11.1 Blindly Buying Tokens Based Entirely on Influencer Recommendations

Influencer promotional threads are frequently paid marketing campaigns, structured native advertisements, or attempts to generate exit liquidity for the influencer’s own low-cost private allocation tokens. Never confuse someone else's paid promotion with rigorous, independent fundamental research.

11.2 Falling for Guaranteed Return Marketing Tactics

Any project, launch interface, or community team that promises guaranteed returns, protected minimum yields, or "assured 10x pumps" is displaying classic fraudulent red flags. Early-stage web3 protocols carry no guarantees; they are defined entirely by capital risk and mathematical probability.

11.3 Reviewing the Public IDO Token Price While Ignoring the Institutional Cost Basis

Evaluating a token's launch price without checking the private venture capital entry valuations is a major analytical mistake. If institutional backers secured their tokens at a 90% discount relative to the public IDO tier, retail participants are walking into a market with massive structural sell pressure.

11.4 Scraping Telegram Communities to Locate Project Domain Links

Searching for official project links directly inside Telegram's public search engine will expose you to an array of fake channels, cloned chat rooms, and imposter customer support handles designed to steal your keys. Always secure verified domain links directly from the project’s official Twitter/X profile or its host Launchpad page.

11.5 Approving Smart Contract Allowances Without Verifying the Domain URL

Malicious phishing domains copy official front-end interfaces flawlessly to trick users into signing malicious contract approval scripts. If you sign an unverified transaction approval on a clone site, a drainer script can sweep all the assets out of your wallet address instantly. Always verify the domain character string before confirming a transaction in your wallet.

11.6 Crowding All Your Liquid Capital into a Single IDO Allocation Round

Early-stage web3 projects face an incredibly high structural failure rate. Even if an allocation appears highly sought-after, it can still lose its value or turn out to be a rug pull overnight. Maintain strict position caps and spread your capital across independent opportunities.

11.7 Ignoring Token Vesting and Cliff Allocations

Many projects only release a tiny fraction of tokens (e.g., 10%) at the launch event, unlocking the remaining supply linearly over an extended timeframe. If the token spot price plummets during those intervening months, your remaining locked tranches will depreciate significantly before you ever have the chance to sell them.

11.8 Missing Contribution Deadlines Due to Inadequate Gas Reserves

Public contribution windows operate on tight schedules and can close within minutes. If you fail to maintain a healthy reserve of the network's native gas tokens (e.g., ETH, BNB, or SOL) to push your transaction through during congestion spikes, your trade will fail and you will miss your allocation slot.

11.9 Chasing Vertical Spikes on the DEX Opening Candle

The first few minutes of a token going live on a DEX are characterized by extreme price volatility as automated sniper bots bid up the price. If you chase these vertical green candles on the public secondary market, you risk buying at an artificial top right before early insiders dump their tokens, leaving you with an immediate loss.

11.10 Holding Tokens of Defunct Projects Indefinitely

Blind community loyalty should never replace objective portfolio analysis. If an asset’s code commits go dark, its developer community disbands, and its trading volumes dry up, cut your losses objectively rather than holding a dying token to zero based on a narrative.

11.11 Confusing the Pre-Sale IDO Price with the Live Secondary Market Opening Price

The public IDO price is the early crowdfunding rate accessible only to a small group of whitelisted users. The secondary market opening price is the live floating spot rate on the DEX. If you buy a token on the open market post-listing, your cost basis is often significantly higher than the IDO rate.

11.12 The Definitive Pre-IDO Investment Self-Audit Checklist

Before risking any capital in an upcoming IDO allocation round, ensure you can clearly answer every single parameter:

- [ ] Can I explain exactly what product or utility service this protocol delivers?

- [ ] Have I independently audited the professional background and identities of the core team?

- [ ] Does the project have a working testnet or functional dApp MVP I can interact with?

- [ ] What real-world utility utility drives the long-term organic demand for this token?

- [ ] Is the launch market cap and FDV realistic when compared against live sector competitors?

- [ ] What was the exact cost basis discount of the institutional seed and venture rounds?

- [ ] Is the vesting unlock schedule fair, protecting the market from early insider dumping?

- [ ] Does the hosting Launchpad have a reliable historical track record of sustainable projects?

- [ ] Has the token and distribution codebase cleared a third-party smart contract audit?

- [ ] Are the liquidity provider (LP) tokens locked inside a verifiable on-chain time-lock?

- [ ] Am I interacting with the verified, official project domain name?

- [ ] Does my wallet hold sufficient native gas tokens to handle severe network congestion?

- [ ] Am I completely prepared to absorb a total loss of my allocation capital?

- [ ] Have I established a clear, disciplined exit and profit-taking framework?

- [ ] Is the size of this investment well within my conservative portfolio risk limits?

If you cannot confidently check off every box on this list, pass on the allocation round or use a tiny position size to learn the operational flows safely.

Chapter 12: IDOs and the DEX Infrastructure Ecosystem

The long-term development of the IDO fundraising model is inextricably linked to the overall health and evolution of DeFi infrastructure. Once an allocation round closes, tokens require deep secondary market liquidity, transparent price discovery, and efficient transaction routing tools to thrive. This is why decentralized exchanges, advanced DEX aggregators, Launchpads, Web3 wallets, cross-chain bridges, and on-chain data monitors form a single interconnected ecosystem.

Protocols like 1inch reflect this technical infrastructure direction. While a DEX aggregator is not an IDO launch platform, it plays a vital role in the post-launch lifecycle of newly issued tokens. As a wider variety of early-stage assets launch natively on-chain, the market's demand for optimized trade routing, minimal slippage execution, deep multi-DEX liquidity aggregation, and cross-chain bridging tools expands significantly.

To expand your understanding of DEX aggregation engines, routing parameters, and Web3 gateway value architectures, analyze the strategic breakdowns hosted on HIBT:

Ecosystem Reminder: Recognizing the structural utility value of decentralized infrastructure does not guarantee that any associated token will experience a market rally. Investors must independently evaluate a protocol's real value capture loops, circulating supply mechanics, macro market valuations, and technical risks.

FAQ: Frequently Asked Questions

1. What is an IDO?

An IDO stands for Initial DEX Offering. It is a decentralized web3 fundraising framework where a project issues and distributes its tokens directly on-chain via a Decentralized Exchange (DEX) or a dedicated Launchpad protocol, with automated liquidity pools opening for live public trading immediately post-sale.

2. How does an IDO differ from a legacy ICO?

An ICO is conducted directly by the project team from their own website with virtually no independent vetting, smart contract oversight, or structural consumer protections. An IDO routes the crowdfunding round through a specialized Launchpad or DEX protocol layer, implementing whitelisting parameters, smart contract validation rules, tier requirements, and automated liquidity injection mechanics.

3. How does an IDO differ from an IEO?

An IEO (Initial Exchange Offering) is hosted completely within the closed infrastructure of a Centralized Exchange, requiring participants to hold verified exchange accounts. An IDO is executed natively on public blockchains via smart contracts, requiring the use of self-custody Web3 wallets, out-of-pocket gas fees, and decentralized exchange liquidity pools.

4. Is profit guaranteed when participating in an IDO?